Editor's Note: Time flies, and as H1 2025 concludes, the metals market has witnessed volatile performance. To help industry professionals and investors review and anticipate market trends, SMM presents this special report on H1 metals market performance for reference!

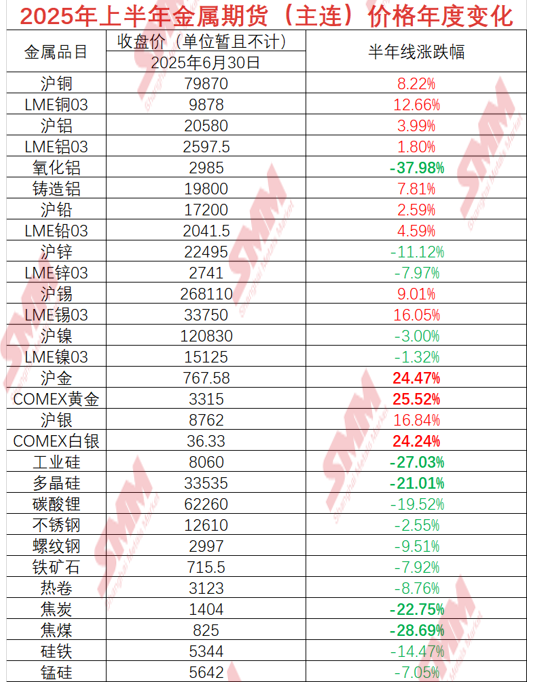

SMM data shows refined cobalt surged 46.19% in H1 2025, becoming the top performer in metals spot markets. SMM #1 antimony ingots and terbium oxide followed closely with 33.21% and 26.16% gains, ranking second and third respectively. Gold and black tungsten concentrate also posted strong performances, both exceeding 20% growth. However, market performances were uneven - the coal sector's overall downturn dragged down grade-I metallurgical coke (dry quenching, nationwide average price) as the worst performer with a 26.34% decline, while oxygen-blown #553 silicon (east China) and germanium ingots fell 24.89% and 15.95%, underscoring significant divergence across metals categories.

Reviewing H1 market drivers, the US dollar index's six consecutive monthly declines provided support for dollar-denominated metal prices. However, frequent adjustments to US tariff policies combined with escalating geopolitical conflicts caused sharp market fluctuations. Meanwhile, notable supply-demand structural changes created stark contrasts with 2024's trends for certain metals. As H2 approaches, market expectations shift anew: intensified domestic policy support is anticipated, Trump-era tariffs' impacts on the US economy may gradually emerge, and the US Fed's subsequent monetary policy trajectory remains under close scrutiny. With these intertwined factors, which metals face violent swings amid exacerbated supply-demand imbalances?

Looking ahead, metals market uncertainties persist. Beyond macro policies and geopolitical factors, emerging industrial demand shifts and supply chain stability will profoundly influence metal price trajectories. Will H1's "star performers" maintain their momentum or experience reversals?

》Click to view SMM Metal Industry Chain Database

Copper

Market sources indicate rumors of an imminent US midterm report on copper tariffs. With accelerated tariff implementation expectations, LME forward curve structures have adjusted, with November-December date spreads returning to flat backwardation. Market expectations for H2 balance have temporarily relaxed. This article assumes July 2025 tariff implementation to analyze post-tariff refined copper balance and structural changes in H2 2025.

From the raw material side, copper concentrates remain relatively tight in the short term, with miners adopting more aggressive Benchmark expectations following production cuts at Kamoa-Kakula due to accidents. Spot TCs also show no signs of recovery. Although Chinese smelters maintain high production supported by long-term contract ore and raw materials, Japanese and Chilean smelters have gradually implemented production cuts or even shutdowns. The tight balance of copper concentrates in H2 is expected to increasingly transmit to copper cathode, with a new round of capacity switching cycle anticipated between old and new capacities.

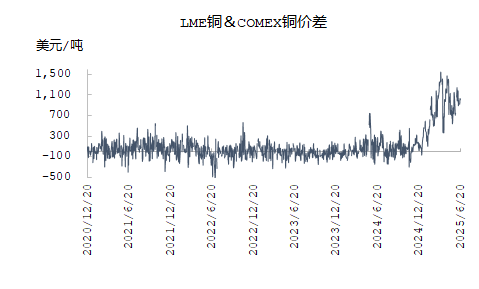

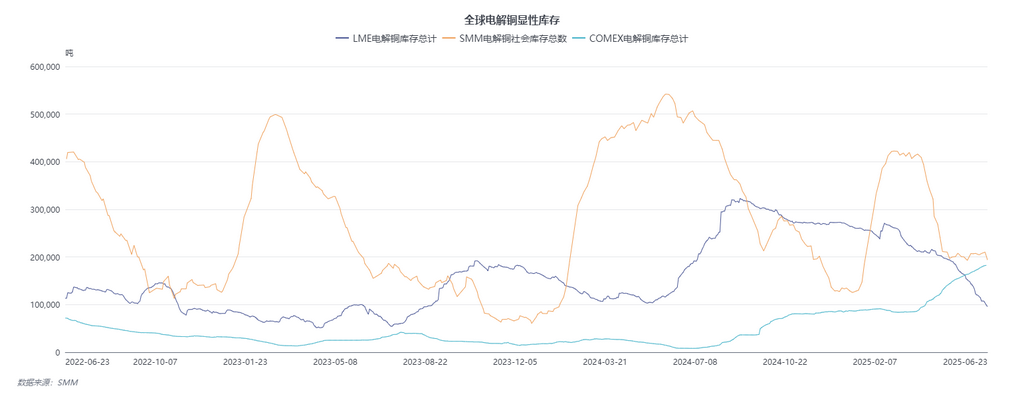

From the copper cathode balance perspective, while apparent copper cathode supply appears surplus in 2025, excluding the LME-COMEX price spread-driven stock diversion to the US, non-US regions - particularly Asia-Pacific - actually face tight conditions. Current LME and Chinese visible inventories have both dropped to around 100,000 mt, with supply pressure continuing to rise in Q4. Regarding global trade flows, Africa still maintains monthly shipments of approximately 20,000 mt of copper cathode to the US, while South America accounts for the majority of US import supply, with China receiving less than 25,000 mt monthly. European demand also diverts part of Africa's copper cathode shipments, with January-May European imports of African copper reaching 90,000 mt, up nearly 40,000 mt YoY. The most direct impact is reflected in China's copper cathode imports: January-May 2025 imports from Africa totaled 559,100 mt (-3.95% YoY), and only 180,100 mt from South America (-52.81% YoY). Consequently, LME Asian copper cathode inventories continue destocking to fill the gap. Meanwhile, persistent maintenance and production cuts at Japan-South Korea smelters have increased Southeast Asia's copper cathode demand deficit, attracting some domestic outflows. 》Click for details

Zinc

►2025 H1 Zinc Concentrate Market Review and Outlook [SMM Analysis]

As 2025 reaches its halfway point, the domestic zinc concentrate market's tight supply situation has eased somewhat. As of June 27, domestic zinc concentrate TCs rose from 1,950 yuan/mt (metal content) at the beginning of the year to 3,800 yuan/mt, while imported zinc concentrate TCs increased from -$20/dmt to $65.25/dmt, with both domestic and imported processing fees climbing steadily.

Limited new domestic zinc mine capacity H1 production basically flat YoY

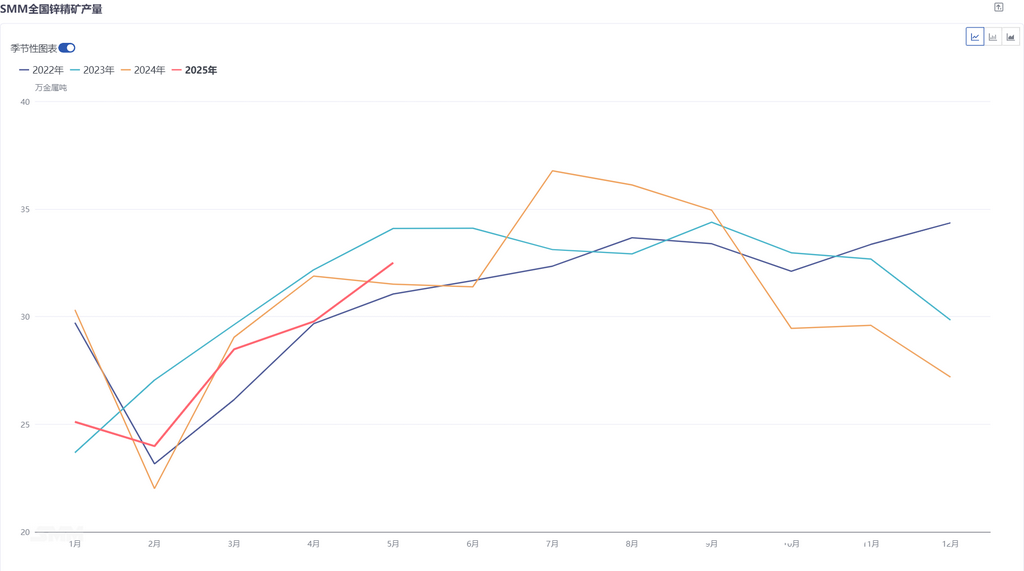

According to SMM data, China's domestic zinc concentrate output reached 788,300 mt from January to May 2025, down 0.06% YoY. In terms of new capacity, some zinc mines commissioned last year continued ramp-up this year, and Huoshaoyun zinc mine began production in May, contributing incremental growth compared to last year. Regarding existing capacity, as the Chinese New Year holiday ended, lead-zinc mines in some northern regions of China gradually resumed production. The overall resumption progress largely met market expectations, supporting a continuous increase in domestic zinc ore production in H1. However, production at some miners in certain domestic regions declined due to disruptions in raw ore grades, coupled with reduced output from some mines nearing the end of their lifespans. With both increases and decreases, zinc ore production in H1 remained largely flat YoY.

Looking ahead to H2, the Huoshaoyun mine continues to ramp up production, bringing a significant increase to domestic zinc ore output. Additionally, June generally marks the tail end of domestic zinc ore production resumptions. Considering the seasonal pattern of domestic zinc ore operations, production at these resumed mines will continue to recover in Q3, while Q4 coincides with the peak period for domestic zinc ore maintenance, coupled with the temporary shutdown of some northern mines at year-end. It is expected that zinc ore production in H2 will first increase and then decrease, possibly reaching its annual peak in July/August.

Newly commissioned and expanded zinc mines are gradually ramping up production. It is expected that overseas zinc ore production will increase by approximately 400,000 mt YoY.

Looking at Q1. According to SMM's production statistics of 20 major overseas miners, based on financial report disclosures, the total zinc concentrate production of these 20 miners in Q1 2025 was 1.297 million mt, an increase of 78,800 mt (6.47%) compared to 1.2182 million mt in the same period last year. The main increases came from the resumption of production at the Tara mine, the ramp-up of production at the Buenavista zinc mine and the Kipushi zinc mine, and the recovery of production at the Antamina zinc mine.

Entering Q2. There were not many disruptions to overseas zinc mines in Q2. Although the Antamina zinc mine in Peru suspended production in April due to an accident, production recovered quickly, and the impact on output was limited. Hudbay Minerals, a Canadian miner, suspended operations at its zinc mine due to wildfires, but due to the good operational performance of Snow Lake since the beginning of the year, it is expected to maintain its full-year operational guidance for 2025. Additionally, Australian miner Polymetals Resources Ltd announced that its Endeavor silver-zinc mine in the Cobar region of New South Wales has achieved commercial production, expected to bring a certain increase in output. SMM expects that with the continuous resumption of production at earlier mines and the ongoing ramp-up of newly commissioned mines, zinc ore production in Q2 will continue to grow significantly YoY.

Significant increases in overseas zinc ore production drive the recovery of China's imported zinc ore volumes.

According to data from the General Administration of Customs, the cumulative zinc concentrate imports from January to May 2025 were 2.204 million mt (in mt), up 52.46% YoY. On the one hand, the significant growth in overseas zinc ore production this year has led to a large influx of zinc ore from mines such as Kipushi, OZ, and Antamina into the domestic market. Additionally, the gradual recovery of domestic smelter production in H1, along with the increased demand for zinc ore raw materials on a MoM basis, has also driven smelters to continuously purchase imported zinc ore to replenish their raw material inventories.

Looking ahead to H2, despite currently weak procurement enthusiasm for imported zinc ore among domestic smelters, the sustained production ramp-up at smelters and the sequential arrival of long-term contracted imported zinc ore shipments procured earlier are expected to maintain China's imported zinc ore volumes at a high level in H2.》Click for details

Steel

►[SMM Hot Topic] 2025 Construction Steel H1 Market Review and H2 Outlook

I. H1 Review

(A) Price Trend Review

Reviewing H1 2025, influenced by macro policy adjustments and sluggish end-use demand, the national average rebar price exhibited a fluctuating downward trend with an overall shift in the price center. Specifically, the national average rebar price reached 3,242 yuan/mt in H1 2025, down 515 yuan/mt from H1 2024, representing a 13.71% YoY decline.

Figure 1: 2025 H1 National Average Rebar Price Trend

Breaking it down month by month: from January to February, as the Chinese New Year holiday approached, market resource circulation largely stagnated except for limited procurement by key ongoing projects. Spot prices stabilized during this period. In March, the conclusion of the Two Sessions brought limited tangible positive news, leading to slightly disappointed market sentiment and weaker price trends. In April, the escalation of Sino-US trade tensions with the US announcing 104% tariffs on China - far exceeding market expectations - spread market pessimism and accelerated steel price declines. May saw tariff negotiations ease, coupled with frequent rumors about crude steel production, which temporarily supported rebar prices. However, the subsequent arrival of high temperatures in north China and rainy season in south China disrupted construction progress, transitioning building material demand into the off-season and maintaining downward pressure on rebar prices.

(B) Fundamental Review

From a fundamental perspective: in January, as the Chinese New Year holiday approached, blast furnace steel mills in multiple regions initiated new maintenance and production controls were implemented in certain areas, while EAF steel mills conducted concentrated annual inspections. On the demand side, market participants and downstream terminals gradually suspended operations for the holiday, with significantly reduced winter stockpiling compared to previous years. With more pronounced demand contraction, inventories accumulated rapidly. In March, downstream sites gradually resumed operations with limited supply growth and sustained demand recovery, causing inventory inflection points to arrive earlier than usual. The construction material sector entered a destocking phase with relatively healthy fundamentals. From April to May, while most blast furnace mills maintained profitable building material production and steel mills in north China resumed production, east China mills prioritized billet orders over finished rebar sales, resulting in stable overall output. On the demand side, downstream feedback indicated persistent funding constraints and slow progress in new project startups, with demand primarily driven by existing projects. This created a weak supply-demand balance and slowed inventory depletion.

As June began, the raw material side continued to offer concessions, and blast furnace steel mills maintained their profits. However, some steel mills adjusted their production structures, shifting towards increased production of specialty and high-quality steel, as well as strip steel. Meanwhile, EAF steel mills faced worsening losses on production, leading to plans for reduced operating hours and even production suspensions. On the demand side, the traditional off-season arrived, and demand remained sluggish. Amidst a simultaneous decline in both supply and demand, the fundamental contradictions in the construction materials market gradually accumulated. According to the SMM survey, as of June 26, 2025, the total rebar inventory stood at 5.1666 million mt, relatively low compared to previous years. However, the trends of in-plant inventory and social inventory have begun to diverge, with in-plant inventory starting to accumulate, increasing by 35,400 mt WoW. Additionally, agents are primarily relying on factory shipments to reduce their own inventory pressure. Therefore, in the short term, the trends of in-plant inventory and social inventory are likely to continue diverging.

Figure 2: National Rebar Total Inventory Trend from 2021 to 2025

II. Outlook for H2

(I) Raw Material Side

In H1 2025, the total supply of iron ore decreased, but with mines expected to come online in H2, the annual increase will primarily be concentrated in the latter half of the year. Furthermore, as the industry enters the off-season, combined with the impact of crude steel production restrictions and subsequent annual maintenance at steel mills, the future supply-demand imbalance is expected to intensify, and pig iron production at steel mills is likely to decline. Therefore, under the scenario of increased iron ore supply and decreased demand, it is estimated that ore prices will be more likely to fall than rise in H2.

In H2 2025, the price center of coke may continue to move downward, but the downward space is limited. On the supply side, coking enterprises have strong production resilience, and unless significant losses occur, it is difficult for coke supply to decrease significantly. On the demand side, the steel industry is performing poorly, with the real estate market sluggish, infrastructure support limited, and the current performance of domestic and external demand in the manufacturing sector remaining unclear, showing a certain degree of pressure. Steel mills are mostly maintaining a low inventory strategy, being cautious about restocking, and purchasing as needed. On the cost side, the growth rate of domestic coking coal production has narrowed, coal mine safety inspections have become stricter, customs clearance at the China-Mongolia border has slowed down, and seaborne coal imports have been restricted, providing support for coking coal prices. In summary, the fundamentals of coke are under long-term pressure, with insufficient upward driving force, but cost support remains, and downward driving force is also insufficient. It is expected that the dry quenching price of quasi-first-grade coke will operate within the range of 1,200-1,400 yuan/mt in H2.

(II) Supply Side

On the supply side, currently, the production profits of some blast furnace steel mills continue to hover around 100 yuan/mt, and short-term production enthusiasm remains high, with no new maintenance plans for the time being. However, some inland steel mills, due to their location disadvantages and high operating costs, are operating at a break-even point or with slight losses. They have already arranged for production cuts or shifted to producing other varieties of steel in the early stages. EAF steel mills have been facing continuous losses on production throughout the year, and some blast furnace steel mills purchase the same types of steel scrap as electric furnace steel mills, leading to continued difficulties in scrap collection. Except for Sichuan, where there are electricity price subsidies during the summer, the operating situation is slightly better. Other regions mainly maintain production during off-peak electricity hours. In the later period, the operating rates of electric furnace steel mills will continue to remain at a medium-low level, with no significant increase expected. 》Click for details

Recommended reading: